China's rare earth restrictions: More collateral damage from US export controls

New Chinese controls are a direct result of US technology policy, whose designers had no plan to address rare earths dependence

China has halted shipments of rare earth elements (REEs) and related materials and products in the wake of the US reciprocal tariffs imposed on April 4. Prices for REE materials have skyrocketed, but in most cases all existing alternative supplies have already been snapped up, and key REEs are not available at any price. While media reports characterize the restrictions as a response to tariffs, the primary purpose behind the retaliation is much different: it is designed to leverage Chinese company dominance of REE supply chains to respond to US export controls and other technology-related restrictions, weaponizing Chinese control in a symmetric manner that mirrors US weaponization of supply chains for semiconductor equipment and advanced GPUs. The huge economic impact of these controls will become increasingly apparent in the coming weeks, despite a lot of irresponsible and unfounded optimism from commentators and casual observers. This will add to the cost of what I have called the “small gain, high cost” US export control measures that began in 2019-2020. What is going on here?

Beijing takes real action in response to US export controls, seeking pain point

China’s April 4 imposition of a global halt on shipments of REEs and products such as REE magnets was proximally related to US reciprocal tariffs announced by President Trump as part of “Liberation Day”—but the real source of the ban was Beijing’s calculus that it needed to inflict real pain on US companies in response to more than two years of US export controls. It will.

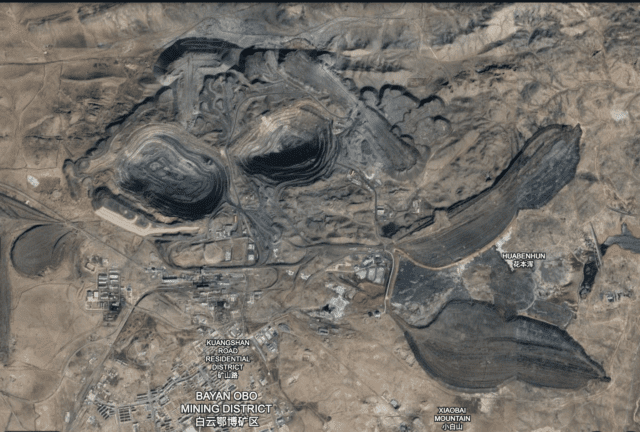

China’s dominance of the REE supply chain, from mining to qualified magnets for autos, is widely known and has been for years. Commentators such as Javier Blas from Bloomberg, who in late April asserted that the impact of China’s REE export controls would be small, because the US “only imports $170 million worth” of rare earths annually, primarily for use in “vacuum cleaners,” will not age well. Nor will other comments from casual observers who think one US company, MP Materials, can solve the problem with a few billion dollars’ investment.

There have been many papers written on the heavy dependence of western supply chains for autos, semiconductors, defense/aerospace, and consumer electronics on Chinese firms that mine, process, and produce finished products from REEs, particularly items such as Samarium Cobalt (SmCo) and Neodymium Iron Boron (NdFeB) magnets used in a variety of end use applications, from missile systems to EVs. In most cases, there are no alternative sources, particularly for magnets and the IP required to make qualified products for regulated industries such as autos. US defense industry firms will be particularly hard hit.

The dependence has been growing for decades, and China in 2010 temporarily restricted exports of REEs to Japan over disputes around the Senkaku (Diaoyutai) Islands. While supply chains adjusted somewhat during this period, the dependence on Chinese firms eventually increased in most areas, particularly with the explosion of green technology industries such as EVs, which are big consumers of REE magnets. One industry observer noted that April 4 was a day he had dreaded for 20 years, because the response from the US government over the past two decades has not had any serious impact on dependence.

Beijing ramps up domestic capabilities to monitor and control REE exports and traders

Beijing has made steady progress over the past five years to gain control and oversight of the sprawling REE upstream and downstream industries. Even before adding many critical minerals to export control lists over the past two years, Beijing had been preparing for the day when it could leverage the dominance of Chinese firms across the sector, covering hundreds of minerals. The 2024 Rare Earth Management Regulations, for example, which took effect in October that year and were likely a direct response to US export controls, introduced a full-lifecycle traceability system and green standards for REE mining and recycling—the Regulations included a dozen technical specifications designed to guide a major shift from high-volume growth to precision oversight.

As part of this campaign, accelerated by the release of US export controls since October 2024, Chinese officials have over the past month launched national efforts to further control critical mineral supply chains and curtail any trading of materials outside central and local government oversight. On May 12, MOFCOM announced a new national campaign to further strengthen oversight of strategic mineral exports, following a high-level meeting in Changsha that included representatives from 11 major central-level ministries, including the Ministries of Public and State Security, along with key provinces that contain major concentrations of critical minerals, including Jiangxi, Hunan, Inner Mongolia, and Yunnan.

Readouts of the meeting suggested that central officials are emphasizing the importance of “full-chain” regulation — covering mining, refining, transport, and export — as a national security priority. As part of this new national campaign, local and central authorities are stressing the need to ramp up compliance training and daily oversight of relevant enterprises up and down the REE supply chain. All provinces were instructed to systematically identify and register firms involved in the export chain, strengthen build-outs of corporate compliance systems, and closely monitor REE resource flows to prevent unauthorized exports.

Chinese media reports have suggested some movement on licenses, citing three specific companies that produce rare earth materials or magnets. However, as of this week the overall number of licenses being released is quite small and most that cite specific end users are for European firms. In addition, reporting suggests that licenses have been granted on a per shipment basis, due to the varying quantities of minerals across shipments. It is now clear that MOFCOM is issuing guidance that companies applying for licenses must ensure that requests for material and magnets are within a particular firm’s historical level of usage and there will be no toleration of efforts to stockpile materials by ordering larger quantities as a hedge. Chinese REE firms and traders are also being advised by MOFCOM not to take orders from new customers. US firms that have gone in and talked directly to MOFCOM appear to be more likely to gain licenses and access REE materials, but even here the volume and time period for resuming shipments remains unclear, as Beijing awaits further progress on the economic and trade negotiations coming out of the Geneva talks.

Beijing will use the REE issue as leverage in trade talks

US officials appear to have been caught off guard by the REE issue, and industry meetings in the runup to the Geneva talks meant that US officials raised the issue with Chinese interlocutors. But there is no indication that Beijing is ready to talk about REE: negotiators at Geneva were clearly not prepared to talk in detail about this issue, and Beijing did not consider the shipment stoppage part of the non-tariff barriers it has eased up on somewhat coming out of Geneva, nor did it indicate any intention to ease up on licensing requirements and the shutdown in shipments of REE materials. Once it is clear in the next few weeks that many companies will be impacted by the restrictions around REEs, with some having to stop production, Beijing will gain considerable leverage that it will want to parlay into a strong negotiating position during the economic and trade talks. It is likely that Beijing will want to bring US export controls into the talks.

The response from Chinese officials at MOFCOM to the Commerce Department guidance on Huawei Ascend 910B, 910C, and 910D processors—asserting that all could have been manufactured in violation of US export controls—was strong, threatening to hit companies supporting implementation of the guidance with penalties under China’s Anti-Foreign Sanctions Law (AFSL). The comments from MOFCOM also linked the Commerce guidance on Huawei Ascends with efforts to constrain China’s development, consistent with the message President Xi Jinping delivered last November at APEC to former President Biden: this is a red line on par with Taiwan, as it impacts China’s future economic growth and Beijing does not accept that this is driven by national security concerns.

This suggests that if the trade talks go off the rails, or the Trump administration ramps up export controls—new Entity List action are being considered, targeting semiconductor firms foundry leader SMIC, NAND leader YMTC, and most significantly DRAM leader CXMT, along with possibly leading AI model developer DeepSeek—Beijing will further tighten REE exports and target US companies. Chalk up all of this to an export control approach which ignored the costs and benefits of each new package of controls. For example, late in the Biden administration, US officials finally acknowledged to their Japanese counterparts that further alignment by Tokyo on export controls would create major risks of retaliation for Japanese firms, including REE export restrictions—but US officials took only marginal steps to help Japan deal with shortages of critical minerals brought on by retaliation from Beijing. This time around, Japanese officials are again in a difficult position, with the global shipment stoppage already impacting the country’s auto industry. Tokyo has been confused by the lack of appreciation of the risks shown during meetings in Washington, where the impression is that no one is in charge of dealing with the issue and there is no long-term strategy, let alone a short-term effort to coordinate around the topic and consider how to approach Beijing.

Beijing’s attempt to bring export controls into the economic and trade negotiations will face an uphill battle, as there will be little support for this from export control proponents in the administration or Congress. But the REE issue cannot be wished away, and Beijing will play hardball. Already there are likely to be no more licenses approved by MOFCOM for export to US military or defense industrial end users, for example—virtually all US missile systems contain SmCo magnets. Expect to see more stories about the issue of the impact of REE magnet shortages on US military readiness in the coming months, along with the usual discussions of increasing deterrence around Taiwan. Chinese media sources are also well aware of the issue, with one leading outlet noting this week that “as of 2024, the U.S. Defense Logistics Agency estimates that current inventories of NdFeB permanent magnets can only support 42 days of wartime demand.” In terms of Chinese firms supplying military end users, “that ship has sailed,” one industry insider told me recently.

Significantly, there has been no serious public discussion of the issue from US officials involved in the economic and trade talks, except a nod from Treasury Secretary Scott Bessent recently that the US needed to reduce dependence on China for these materials. No official has talked about realistic time frames—a minimum of five years in most cases—or the costs of building an alternative end-to-end supply chain. According to one industry observer: “There is no plan. This is an abject failure of vision.”

As stockpiles at many companies run out over the coming weeks and production halts are announced, including in Europe, Japan, and South Korea, the scope of the problem and the collateral damage will become clearer. Wolfgang Niedermark, an executive board member of the Federation of German Industries (BDI), stressed in mid-May that “the window to avoid significant damage to production in Europe is rapidly closing.”

The costs of the “small yard, high fence” and broader Sullivan Doctrine will continue to mount in the coming months, adding to the massive costs to companies such as Nvidia over the past several weeks alone—in the tens of billions of dollars. Nvidia CEO Jensen Huang last week slammed US export controls as a major failure, and he was not even talking about the secondary and tertiary collateral damage that is now apparent. China observers calling for tightening controls do not seem to have factored in REEs and other levers Beijing could choose to use against US companies, nor the broader risks around the current focus on slowing China’s AI development.

One point of clarification - USTR Greer was asked about rare earth export restrictions on his return from Geneva and said “Yep, the Chinese have agreed to remove those countermeasures. If they don’t do those things, we’re going to be back in a different situation. But I expect they’ll remove them.” The lack of flow of rare earths to the US is going to become a bone of contention soon.

Also, while I don't doubt your analysis that we are likely to encounter significant supply chain problems resulting from shortage, given the lack of progress in addressing this well known vulnerability since 2010, perhaps having a crisis is the only way to generate action to address it.